The following analysis is market information about greater Minnesota apartment trends based on observations compiled by Mitchell Simonson, MAI.

Greater Minnesota – 2018 Apartment Trends

Over the past 12 months, I have appraised numerous greater Minnesota apartments ranging in size from about 20 to 150 units. The geographic region has spanned the “banana belt” surrounding the Minneapolis/St. Paul metropolitan area. The primary cities forming the “banana belt” include Rochester, Mankato, St. Cloud and Duluth, as well as smaller rural towns in between. This allows us to complete in-depth analysis of historical income and expense statements on completed assignments. Additionally, our firm supplements the internal observations and data by constantly interviewing apartment owners, brokers, property managers and lenders.

The following discusses general rent, vacancy, operating expense, and capitalization rate trends in greater Minnesota. A quick overview of each is summarized below, followed by more details.

Rents – Generally speaking, rents remained strong in 2017, with most communities able to increase rents. The exception is Fargo/Moorhead as most apartment property managers are now offering free month rental incentives.

Vacancy Trends – Vacancy rates in communities such as St. Cloud, Mankato, Rochester, county seats and smaller communities remained quite low. Fargo/Moorhead is experiencing significant over supply and vacancies have climbed north of 9.9%.

Operating Expenses – Operating expenses in greater Minnesota have held pretty stable. With rising sale prices, real estate taxes continue to be a concern for property owners.

Cap Rates – Cap rates appear to have remained relatively stable in 2017, with some compression in the larger communities.

Rent Trends – The quick story here is rents continued their upward ascent that has now been in place for several years in the greater MN apartment market. Overall, low vacancies and steady renter demand allowed owners and managers to implement one or more rent increases. However, not all properties are operated and managed the same and some owners tend to be more conservative with regard to rent growth.

Vacancy Trends – In 2017, it seemed nearly every greater Minnesota community surveyed with the exception of Fargo/Moorhead had stabilized vacancy rates (less than 5%). According to data compiled by Fargo appraisal firm Appraisal Services Inc., the current vacancy rate in Fargo-Moorhead metropolitan area is 9.91%. This represents a slight increase from 9.21% one year ago. The following table shows the quarterly vacancy rate and number of units under construction in the Fargo-Moorhead metropolitan area over the past five years.

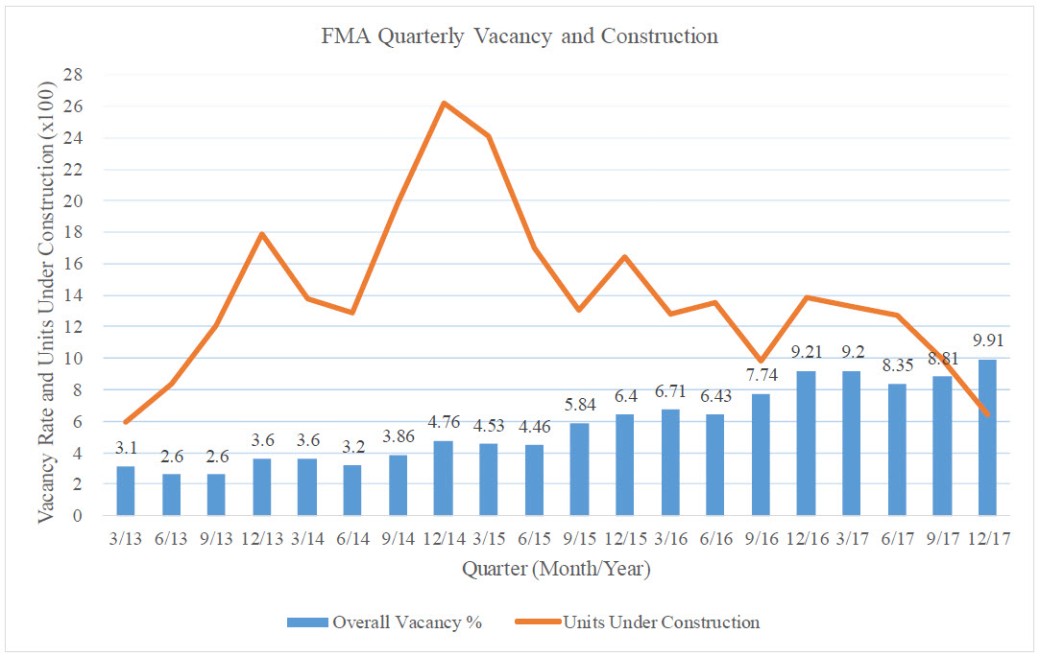

Source: Appraisal Services Inc

Over 6,000 units have been added to the Fargo market area since 2013, when vacancy rates reached a floor of 2.6% metro wide.

The low vacancy rates across most of greater Minnesota are attributable to favorable employment and economic trends and rental rates that remain below levels necessary to support new construction costs. The larger markets such as Rochester, Mankato, St. Cloud and Duluth have seen new apartment development. Similar to last year, most participants do not anticipate significant changes in vacancy in 2018.

Operating Expenses – Real estate taxes are generally cited as the one major area of concern. As values have increased over the past few years and sales become available, this tends to be the one consistent expense line item that is of concern to investors. Utility expenses tend to increase annually. A review of historical operating expenses for most properties suggests relatively stable expenses for other line items. With low vacancies in most markets and steady rent increases, operating expense ratios have stayed flat or decreased. Rising labor and maintenance costs have reportedly been a concern in Minneapolis/St. Paul metro area properties, but not as much in outstate areas.

Capitalization Rates

Capitalization rates appear to have remained relatively stable in 2017, with some compression in the larger markets. It has been evident over the past several years that more buyers are searching for investment opportunities beyond the Minneapolis/St. Paul metro area. Higher quality apartments in the larger communities (such as Fargo, Mankato, St. Cloud, etc.) are in the approximate range of 6.00% to 7.00%. Rochester and St. Cloud have seen a few larger, newer properties trade with cap rates below 6.0%. Cap rates for average-to-good quality properties in smaller communities generally range from about 6.75% to 7.75%. Properties with some level of deferred maintenance and/or older properties tend to sell at cap rates of 8.00% and above. Of course, each property is unique and must be analyzed independent of the general market parameters.

Most market participants report general optimism for continued strength in the greater Minnesota apartment market, particularly with a stable tenant base.

What are your expectations for greater MN apartment activity in 2018?

Are you looking for information on valuation trends in Minneapolis/St. Paul metro area? This link can help you: https://simonsonrealestate.wordpress.com/2018/01/23/minneapolis-st-paul-2018-commercial-real-estate-valuation-trends

Mitchell Simonson, MAI is an expert commercial real estate appraiser and investor. Since 2005, Mitchell has appraised hundreds of commercial real estate properties across many property types.

Real estate is a great vehicle to create long-term wealth! He speaks, consults and trains on Helping Lenders, Brokers and Investors Navigate the Appraisal Process and to ensure his clients are making wise commercial real estate investment and underwriting decisions to help them meet those goals.

To inquire about booking Mitchell for consulting or appear at your next conference or event, please email mitch@simonsonap.com or call at 612-618-3726.